Planning For Your Future

Wealth management is more than advice relating to investment options. It is a holistic approach to managing your financial health and starts by us taking the time to fully understand the goals you have for you and your family. Whether they are:

- Retirement

- Helping your family

- Preserving your wealth or

- Giving back

We will work with you to answer your questions and prepare a plan to help you achieve your goals.

Financial Planning Blogs

New and Improved – Savings plans get even better

The past year has seen the addition of a new registered plan aiming to help first-time home buyers, as well as increased annual contribution limits for both the Tax Free Savings Account and the Registered Retirement Savings Plan driven by inflation. In light of these changes, this article will provide an update of the various registered savings plans available in Canada.

Getting Wealthy and Staying Wealthy

Everyone worries about money. Daniel Kahneman, a behavioural economist and winner of the Nobel in economic science once said “Money does not buy you happiness, but lack of money certainly buys you misery”. Money worries are the greatest source of stress, more than work, personal health and relationships.

Don’t Hesitate; Just Designate

Designating a beneficiary on your registered accounts is one of the most important decisions in estate planning. By designating a beneficiary, you inform the financial institution of your plans for your estate after your death. While it is a simple act requiring little in the way of paperwork, it can do a great deal of heavy lifting in establishing your wishes for your estate and ensuring your assets are distributed according to your wishes when you die.

Knowledge is power

s the great Francis Bacon proposed, “knowledge is power”. If so, then so too must be saving and sponsoring another person in their pursuit of that knowledge. The Registered Education Savings Plan is a highly effective vehicle for Canadians to save for the education of a loved one, chiefly children and grandchildren.

TFSAs – The magic of tax free compounding

How large can a TFSA get? It depends, of course, on the rate of return and the number of years that compounding has to work its magic.

Donating Securities to Charity – The Angel is in the Details

This is a follow-up to my earlier post on donating securities to charities. In short, making a charitable donation using securities – such as shares of public companies – that have appreciated in value is a highly tax-efficient strategy. This article will go into greater detail about the tax implications of the strategy.

Tax Free Savings Accounts – Flexible, easy and really and truly tax free

Often, our clients ask us how we can help them and their children invest in a tax effective way. There are not very many ways to do that in Canada. While many are familiar with RRSP accounts, TFSA accounts are of great benefit as well. TFSAs are only available to Canadian residents who turned 18 on or after 2009. They allow for capital gains, interest, and dividend income to be (and grow) tax free. Unlike RRSPs and many other registered accounts, TFSAs also offer flexibility.

Financial Planning at Baskin Wealth Management

Financial planning can seem like a nebulous concept. Because it touches on many aspects of a person’s financial life – investing, retirement planning, tax planning, estate planning, and insurance – its holistic nature is in fact one of its key strengths. Sound analysis of a person’s financial situation requires a strong understanding and analysis of each of these areas and the ability to analyze each simultaneously.

Charitable donations using securities

Making a contribution to a charity by way of gifting securities which have appreciated in value is a simple, easy and highly tax-efficient strategy. We recommend making use of this strategy to all our clients who have non-registered assets and who wish to make significant gifts to a registered charity.

The kids will be all right – How to save for your kids’ and grandkids’ futures

Generous parents and grandparents frequently look for the most beneficial ways to give their descendants a head start, often by putting funds aside in an investment for their benefit. This has perhaps become more common during the pandemic, as those who have been fortunate enough to have continued employment, and retirees, have seen their expenses decline with a corresponding rise in their savings. There are a number of different approaches available, each with its own pros and cons, and this article will expand on each.

OAS – To Delay or Not

An important topic for our clients nearing the age of 65 is how to best structure potential income sources during the retirement years. Timing of Old Age Security (OAS) benefits will be considered in the context of such discussions.

How interest rates affect the decision to borrow vs. save

In Benjamin's last blog he examined the framework for determining whether one should use cash to pay down their debt, or to build their investments. While the framework necessarily includes analysis of current interest rates, one factor that was not considered was how interest rates will change over the lifespan of your debt. This article will examine these considerations.

Frequently Asked Questions

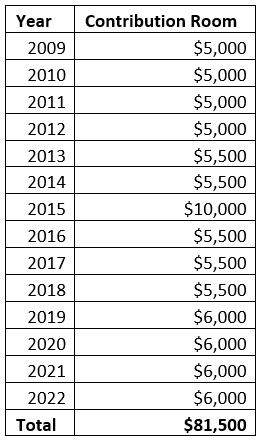

A Tax-Free Savings account is a type of account available to Canadians to help them save for retirement, a major purchase, or any other kind of saving. Each Canadian resident age 18 or over receives contribution room annually that can be used at any time; it does not disappear if unused. If you turned 18 in 2009 or earlier and were a resident of Canada since that time, you have $81,500 of total TFSA contribution room as of 2022; in 2022, the annual contribution room was $6,000 and a list of contribution amounts by year is available here and below. The benefit of investing inside a TFSA is that there are no taxes due on investment income of any kind, nor are there taxes on withdrawal. Once the money has been deposited in the TFSA, it is truly tax-free.

TFSAs are very efficient savings vehicles given their complete tax-sheltering status, and since there are no penalties for withdrawals, they are quite versatile and can be used for short- or long-term saving. If you withdraw funds from your TFSA, you regain the withdrawn contribution room up to your lifetime maximum, but only on January 1st of the following year. So, if you withdrew your entire $100,000 TFSA on June 15th, 2019, you got all your contribution room back plus the new contribution room for 2020 on January 1st, 2020.

The main limitation is that allowable contribution room for TFSAs is small relative to the retirement portfolio a family would need, absent significant pension income.

A Registered Retirement Savings Plan is a type of account available to Canadians to help them save for retirement. Each Canadian who earns income receives contribution room of up to 18% of your earned income from the previous year, reduced if you are a member of a defined benefit pension plan, that can be used at any time; it does not disappear if unused. If you earn about $162,000 per year or more, you can contribute the maximum yearly amount, which is $29,210 as of 2022 and generally increases by a few hundred dollars yearly. Just the act of contributing to the RRSP has benefits, and you can hold most types of publicly traded investments inside an RRSP, which has further advantages.

These are the two main benefits of investing through an RRSP:

- When you make a contribution, you get a tax deduction equal to the amount you contributed. So, if you contribute $10,000 to an RRSP, you reduce your income for that year by $10,000, and receive a reduction in taxes based on your tax rate – the higher your income, the bigger the reduction.

- While the funds are in the RRSP, you do not pay any tax on capital gains, interest, or dividends. This is known as “tax-sheltering”. This allows the investments to grow more quickly, since the profits are not eaten up by taxes until the money is withdrawn.

However, when you eventually withdraw money from your RRSP, you must pay income tax on any amount withdrawn. For most people, you will earn less money – and thus have a lower tax rate – in retirement, so you will pay less tax overall by using an RRSP.

Using a Spousal Retirement Savings Plan (Spousal RSP), a higher-earning spouse can pay less tax by investing in the name of their spouse or common-law partner. The high-earner makes the contribution and therefore benefits from the reduction in income for that year and, when the funds are withdrawn at retirement, they are taxed in the hands of the lower-earning spouse – this is a technique known as income splitting.

In the year that the RRSP holder turns 71, they must convert their RRSP to a Registered Retirement Income Fund (RRIF), which means that no new contributions are allowed and they are required to start withdrawing, and paying income tax on, a small percentage of their RRIF assets every year starting the following year (in which they turn 72). The withdrawal rate starts at around 5.5% per year at age 72 and increases yearly, up to 20% at age 94 and beyond; full minimum withdrawal rates are available here. RRIF holders who have a spouse or common-law partner can also elect to use their partner’s age for calculation of the minimum withdrawal, in order to reduce the size of the mandatory withdrawals.

Money that you contribute to your RRSP is not locked in. You can withdraw it at any time if necessary, but you will have to pay income tax on the withdrawals, and the contribution room used when you made the original contribution is lost – funds in an RRSP are intended to remain there until retirement. However, if you are using money for first-time purchase of a home or for post-secondary education, you can take up to $35,000 or $20,000, respectively, as long as you agree to pay back the amount withdrawn over the following several years; there is no tax deduction for the repayments.

For many Canadians, the RRSP is the primary savings account they’ll use to save for retirement. An RRSP for a diligent saver who starts early and puts their money to use by investing can grow to millions of dollars by retirement.

This is a very common question because the two programs have many similarities, but also a few key differences. In general, TFSAs are more appropriate for people who expect their incomes to rise over time (often, young people), whereas RRSPs are more appropriate for those with already high incomes or who expect to see their incomes stay the same or decline.

Here are the primary differences between the accounts:

- The RRSP tax deduction is a very important element of the plan. For most people, it allows for tax minimization by delaying tax remittance from working years, when incomes and tax rates are higher, to retirement years, when incomes and tax rates are lower. This deduction becomes more beneficial as a person’s income and tax rate increases. A person with a marginal tax rate of 50% who makes a $20,000 RSP contribution receives a $10,000 refund; a person with a marginal tax rate of 20% who makes the same contribution receives a refund of only $4,000.

- It is possible for some people – diligent savers, high earners, and people who will receive large inheritances or gifts – to have higher incomes in retirement than in their working years. As a result, some people will end up paying more taxes when utilizing the RRSP than not.

- Neither RRSP nor TFSA contribution room disappears if unused. As a result, if a person expects their income to increase significantly in the short-term, it can be advantageous to hold off on RRSP contributions until the deduction becomes for valuable, and to make TFSA contributions in the meantime instead.

- TFSAs are versatile. Money can be deposited and withdrawn with few restrictions. This means the TFSA can be used to save for major purchases, such as buying a home, while allowing the investments to grow tax free, and full contribution room will be restored on January 1st of the year following any withdrawals. On the other hand, RRSPs are less versatile. Since all withdrawals are fully taxed as income, unanticipated withdrawals during working years can be taxed heavily. As well, the contribution room originally used is permanently lost on withdrawal.

In short, here are the three major factors and their impacts on the decision.

- Income today vs. in the future

- Expect to have higher income in the future? TFSA is relatively more attractive right now.

- Amount of savings room available

- For most people, the TFSA has substantially lower lifetime contribution room for most people, so it is maxed out more quickly.

- Whether flexibility is important

If the funds might be required for something other than retirement, the TFSA is more appropriate.

A Registered Retirement Income Fund (RRIF) is the second stage in an RRSP’s lifetime, during which the holder must withdraw a minimum amount from the account annually.

An RRSP can be turned into a RRIF at any time, but it must be completed by the end of the year in which the holder turns 71. Regardless of the holder’s age, RRIFs have required withdrawals which must be taken starting the year after the RRSP-RRIF conversion, and each dollar withdrawn is taxed as income. These required withdrawals are based on a percentage of the assets in the RRIF at the beginning of the calendar year, and increase over time, and increase more sharply past age 72 (about 5.5% per year at age 72. Full minimum withdrawal rates here: https://www.taxtips.ca/rrsp/rrif-minimum-withdrawal-factors.htm). By age 94 and beyond, RRIF holders must withdraw 20% each year. RRIFs can be converted back to RRSPs any time before age 72, but past age 72 they must remain as RRIFs permanently.

There are a number of other important differences between RRSPs and RRIFs.

- Money cannot be deposited into a RRIF.

- If the financial institution has not been provided withdrawal directions by year-end, they will generally process a lump-sum withdrawal for the minimum withdrawal amount in December and remit to the holder by cheque or electronic payment.

- Except for amounts below the required minimum withdrawal, financial institutions are required to withhold some percentage of the withdrawal for taxes and remit to the CRA. The withholding tax percentage depends on the size of the withdrawal, and RRIF holders can choose to withhold more (but not less) than the required withholding tax rate. The withholding tax serves as a way to smooth out many RRIF holders’ taxes to prevent a large tax bill at year end. However, the withholding tax system is imperfect; holders of large RRIFs with little other income can end up withholding too much tax and receiving a large refund at year end. Holders of RRIFs who also have significant pension or employment income may be well served by withholding more than required to smooth out their tax payments.

A Registered Education Savings Plan is the primary tool available to Canadians to help them save for education expenses. An RESP is most commonly used for the benefit of children or grandchildren, though they can be used for anyone, including immediate family members – for clarity, referred to as “students” in this post.

An RESP has two primary benefits. First, like an RRSP or TFSA, the funds inside an RESP are tax-sheltered. This means that there is no tax on the investment income earned as long as it remains in the plan. This allows the investments to grow more quickly as the growth is not eroded by taxes – though there are taxes due on withdrawals, which we’ll get to later. The second benefit is that contributions to an RESP are partially matched by the government, increasing the value of any contributions made.

There are a number of important points to keep in mind about the RESP:

- If your family income is $100,392 or higher, the government grant is 20% of the value of your contribution, up to a contribution of $2,500 per year, per student, equalling $500 grant per year per student. If family income is lower than $100,392, the first $500 are matched at a higher percentage, according to the table below.

- Grant is determined on a calendar year basis, and only one missed year of grant can be made up per year. If not making up for a missed year, you can contribute more than $2,500 (up to the lifetime maximum of $50,000 per student), but you will only receive grant as if you contributed $2,500

- Depending on your family income and the number of children you have, you can also qualify for the Canada Learning Bond, which is a one-time government contribution towards an RESP. For most families, family income needs to be below $50,000 to $60,000.

- The RESP is flexible with regards to approved post-secondary education. Universities, colleges, and trade schools, whether in Canada or elsewhere, all meet the criteria. Part-time study is also permitted as long as the student spends 10 or more hours per week on the program or coursework.

- Generally, RESP funds can be used to pay for any expense assuming the student continues to be enrolled, including tuition, textbooks, rent, food, etc.

- If withdrawals are very large, the financial institution administering the RESP might request documentation or receipts detailing the expenses.

- The financial institution tracks the values of contributions, grants, and investment earnings in the plan as they are taxed differently. Contributions are non-taxable on withdrawal, and grants and investment earnings are taxable as income for the student, who generally pays little or no tax given their income.

- If the student decides not to attend a post-secondary institution, there are a few options. If there are other students (usually siblings) in the RESP, then the funds can be used for the siblings’ education. If that’s not possible, and the RESP must be collapsed or withdrawn from early, then each type of funds within the RESP are treated differently:

- Any grant or bond received is forfeit and returned to the government.

- Contributions are returned to the RESP holder (usually parents) tax-free, as the contributions were already made with after-tax money.

Investment earnings, or profit, are taxed as income plus an additional 20% penalty. If you have the RRSP contribution room and meet a few criteria, up to $50,000 can be rolled into an RRSP without being hit with taxes on those amounts.

Canada Pension Plan or CPP refers to the government run pension for Canadians who have earned employment income throughout their careers. Most people who have worked for many years in Canada, or a country with a social security agreement, can expect to receive between a few hundred to a little over a thousand dollars per month when they begin payments, for which the standard age is 65, until their death. Payments are fully taxable as income and can be partially or fully split with a spouse or common-law partner subject to restrictions. Residents of Quebec have an analogous program called QPP.

One aspect of CPP which receives considerable attention is the ability to take payments up to 5 years before or after the standard age of 65. Taking payments early permanently reduces the size of each payment, and delaying payments permanently increases their size. Much has been written about the pros and cons of taking CPP earlier versus later; you can find our analysis on the topic here. In short, if you are struggling to make ends meet, delay CPP as long as you are able. If you don’t need your CPP payments to help you with expenses, then taking around age 65 is generally best, though it depends on your health and your assumption for future investment returns.

The precise calculation for CPP payment eligibility is fairly complex and its intricacies are beyond the scope of this article. The basics are that a Canadian who has lived and worked in Canada for around 35 years or more, earning over $65,000 per year in today’s currency would be eligible for the maximum payment amount – about $1,250 per month or $15,000 per year at age 65. However, very few Canadians actually receive the maximum as a result of not working long enough or low earnings, particularly early on in one’s career. The average monthly CPP payment is about $727 or $8,700 per year, which is only 58% of the maximum.

CPP payments can be split with one’s spouse or common-law partner subject to some restrictions. The longer you and your spouse were a couple during the CPP contribution years, the greater share of the CPP payments that can be split. So if you contributed to CPP for 30 years, and have been with your common-law partner for 15, you can split half of your CPP payments, but the rest is still attributable to you. In this case, 75% of your payments would be attributable to you and 25% to your spouse (since you split half of the payment in two, 25% remaining with you and 25% going to your spouse).

The Canada Pension Plan also administers several other programs which are used to benefit spouses of deceased CPP contributors, children of deceased or disabled CPP contributors and also a one-time death benefit towards a contributor’s estate. The Government of Canada website has very good summaries of these programs on their website.

Old Age Security or OAS is a supplementary income program for Canadian residents ages 65 and older with moderate or low individual income. Unlike CPP, its eligibility is based only on years of Canadian residence, not employment income. OAS payments are generally smaller than CPP with a maximum of about $7,000 per year, they are also fully taxable and subject to a special tax, known as a “clawback”, if the recipient’s individual income exceeds a certain level. Similar to CPP, OAS can be delayed past age 65, to a maximum of age 70, with each month’s delay increasing the payment amount by 0.6% or 36% if payments are delayed to age 70.

As of July 2022, seniors age 75 or above had their OAS increased by 10%.

The clawback is the most complex part about receiving OAS, and also the main feature which allows for some measure of planning and optimization. An individual with income below $81,761 as of 2022 receives the full OAS payment amount. For every additional dollar of income above that figure, 15 cents of OAS is clawed back in the following summer (OAS is administered on a 12 month schedule from July to June). As a result, if individual income is above $134,253, the entirety of OAS is clawed back for the year (or $136,920 for seniors 75 or older).

The main source of optimization surrounding OAS is to reduce income into, or below the threshold for a particular individual in a year. If a person’s income is near one of the thresholds, it could be valuable to, say, use capital losses to offset capital gains in order to allow for some or all of the OAS payments to be received without clawback. However, it’s important to remember that all income, including OAS, is taxable as income, and tax minimization is also very important. A focus on simply maximizing OAS payments can result in higher taxes payable and actually mean less after-tax income.

OAS also has additional programs for people with low incomes (the Guaranteed Income Supplement or GIS), a program for people not yet old enough to receive OAS but whose spouses already receive the GIS, and a program for widowed people ages 60 to 64. The Government of Canada website has very good summaries of these programs on their website.